Resilience rises on the food and fibre agenda

KPMG’s Agribusiness Agenda 2026 urges directors to focus on adaptation, systems thinking and long-term value.

Boards connected to New Zealand’s food and fibre sector should be paying close attention to KPMG’s newly released Agribusiness Agenda 2026. Resilience, adaptation and long-term systems thinking now belong in core governance conversations.

Ian Proudfoot, KPMG’s global head of agribusiness and author of the Agenda, says the shift reflects the realities already facing the sector.

“Sector leaders have told us that incremental change alone will not be sufficient to create an aspirational future for the food and fibre sector,” says Proudfoot. “Intentional, non-linear change is now required.”

Global disruption tests the sector

The Agenda describes a sector operating in a volatile and fragmented global environment, where food systems are tied to national security and strategic resilience.

Alongside climate volatility and changing consumer expectations, the report highlights ‘future shapers’, including geopolitical fragmentation, constrained insurance markets, cyber insecurity, energy affordability, trade disruption, AI, water scarcity and growing competition for strategic resources.

Food systems are being viewed globally as key contributors to national security and strategic infrastructure, with implications for market access, supply chains and operational resilience.

Proudfoot says geopolitical tensions, energy price volatility and supply chain disruption featured strongly in industry discussions during development of the report, reinforcing the importance of resilience.

Directors need to look beyond operational risk and consider how fragmented markets and interconnected systemic risks could affect strategy, investment and resilience. Against that backdrop, resilience has become a core strategic and economic imperative.

Resilience moves to the centre

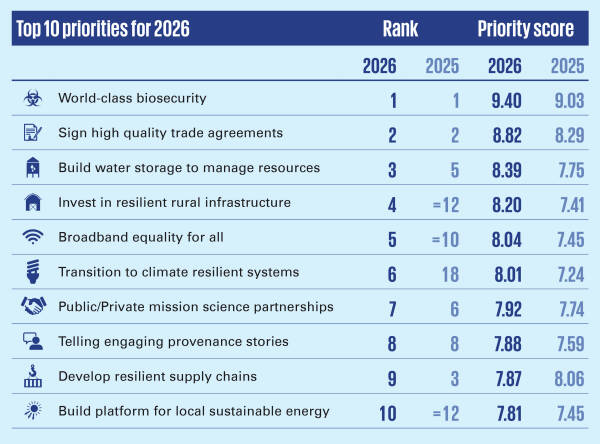

One of the clearest themes in this year’s Agenda is resilience becoming a strategic priority.

Three of the top 10 priorities identified by sector leaders refer directly to resilience: resilient rural infrastructure, climate resilient systems and resilient supply chains. Water storage and local sustainable energy also show a growing focus on adaptation and system resilience.

Source: KPMG Agribusiness Agenda 2026

Two years ago, transitioning to climate resilient systems ranked last among all priorities surveyed. In 2026, it made its first appearance in the top 10, showing how rapidly climate resilience has re-emerged as a strategic concern.

Proudfoot says recent disruption has sharpened industry thinking. “Having had a more stable period over the past 12 months, the Iran conflict has returned us to uncertainty, instability and shock.”

Industry leaders, he says, recognise that resilience cannot be treated as a standalone sustainability initiative.

“People were starting to recognise that we cannot continue to just accept that weather events occur and then we build back. We need to start to get ahead in terms of how we plan for those events.”

Boards should test long-term asset resilience, operational continuity and investment priorities.

Nature and environmental action become strategic

The Agenda sets out a broader shift in how environmental priorities are understood. Environmental action is now linked to resilience, competitiveness and long-term economic performance.

Proudfoot says organisations are assessing environmental action through both resilience and commercial lenses.

“People will act if their investment makes economic sense,” he says. “Thinking about it through the lens of the chief financial officer in terms of the actions we take is as important as thinking about it through the lens of the chief sustainability officer in an organisation.”

That framing is likely to resonate with boards focused on resilience, capital allocation and long-term value creation.

The report also highlights the strategic importance of nature-based systems, including water, biological resources and ecosystem resilience.

“Water ultimately . . . is New Zealand’s liquid gold,” says Proudfoot. “In a water-scarce world, our ability to capture and use our water is going to be a significant competitive advantage.”

Continuous change, not a linear transition

A theme running throughout the Agenda is that change is unlikely to follow a smooth or predictable path.

Proudfoot says leaders recognise the pathway to a more resilient and competitive food and fibre sector is unlikely to be linear. “Change is going to be continuous. We’re going to go down some rabbit holes. We’re going to make some massive jumps forward.”

This has implications for governance capability, strategy oversight and organisational culture.

The report suggests boards may need to govern through uncertainty, experimentation and adaptation, rather than assume stable transition pathways.

Proudfoot argues leadership will be critical, saying: “We need leaders that are prepared to stand up, take the risks and drive us forward.” That includes being willing to move before all answers are known.

“We don’t have the time available to be perfect,” he says. “We have to be prepared to accept the adequate and move forward.”

Energy, infrastructure and future competitiveness

This year’s Agenda also places energy resilience and local sustainable energy among the sector’s top priorities.

Proudfoot says leaders recognise that future resilience may sit as much within farm systems as outside them.

“There is this growing global recognition that potentially a large part of the answer to energy issues sits inside the farm gate rather than outside,” he says.

“How can we use the biomass in farming systems? How can we use the land available in farming systems to both help lift the resilience of farmers, their economic resilience, and ensure we’re thinking about the future of food, farming and fuel?”

The report also highlights infrastructure as a growing governance concern – from transport and connectivity through to social infrastructure and workforce capability.

“There was this unique consistency of views around what is important,” Proudfoot says of this year’s findings.

Climate resilience, infrastructure dependency, nature, energy and market expectations are connected governance challenges facing the food and fibre sector.

A governance challenge

Although much of the Agenda focuses on operational pressures and sector transformation, it also raises important questions for governance.

Notably, executives again ranked accelerating the net zero transition higher than directors did, suggesting a possible disconnect between operational leadership and board-level strategic focus.

The report also identifies growing expectations from markets, customers and global trading partners, where resilience, climate adaptation and environmental performance are tied to long-term competitiveness and market access.

As climate volatility intensifies and markets evolve, boards are likely to face growing pressure to connect short-term adaptation with more integrated system-level thinking.

“The future will be shaped by the leadership that we have in the sector,” says Proudfoot. “And the leadership we’ve got . . . is committed and ready to lead a journey of change.”

Now in its 17th year, KPMG’s Agribusiness Agenda draws on nationwide roundtable discussions and survey responses from directors, executives and industry leaders across the food and fibre sector.